Scope 3 emissions, explained

Value chain emissions in scope 3 are challenging – but vital – for businesses to address.

Scope 3 emissions are all the indirect greenhouse gas emissions that occur across your value chain, both upstream (your supply chain) and downstream (customers, end-of-life), from sources you don’t directly own or control. Also called value chain emissions, they account for, on average, between 70-90% of a company’s total emissions, according to CDP. The Greenhouse Gas Protocol defines 15 categories of scope 3 emissions spanning everything from purchased goods to employee commuting to how customers use and dispose of your products.

Scope 3 greenhouse gas (GHG) emissions, also known as value chain emissions, are increasingly at the centre of corporate climate strategy. As companies work toward net-zero targets, tackle unintentional greenwashing, and respond to growing regulatory and investor pressure, scope 3 is often where most of the work lies.

Here is what scope 3 emissions are, why they matter, and how businesses measure, manage, and report them.

What are scope 3 emissions?

Scope 3 emissions are all indirect emissions that occur in a company’s value chain and that are not already included within scopes 1 or 2. They are also known as value chain emissions.

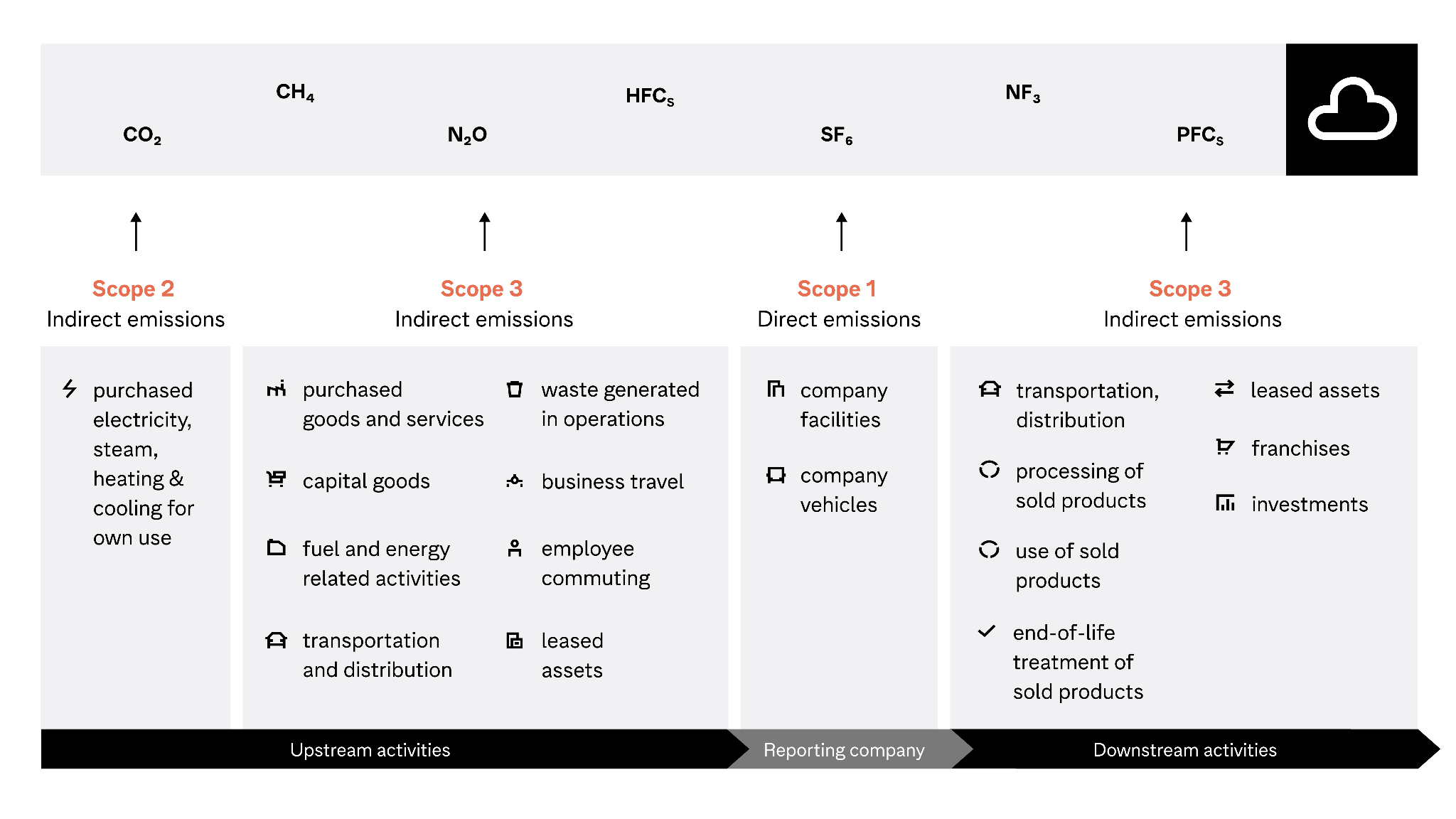

The Greenhouse Gas Protocol (GHG Protocol) – the most widely-used framework for calculating corporate greenhouse gas emissions, defines scope 3 as other indirect emissions outside a company’s own operations and purchased energy. It divides these into 15 categories, split between upstream emissions (from your supply chain) and downstream emissions (from how your products are used and disposed of).

Scope 3 carbon emissions include everything from the extraction of raw materials by your suppliers, to the energy customers consume when using your products, and the emissions generated when those products are discarded at end of life. Consequently, scope 3 is, for the majority of companies, by far the largest source of emissions. According to CDP data, corporate businesses are reporting their supply chain emissions to be 26x greater, on average, than their combined total across scopes 1 and 2. Let’s look into it in more detail.

What are the 15 scope 3 categories?

The GHG Protocol’s Corporate Value Chain (Scope 3) Standard identifies 15 scope 3 emission categories.

| # | Category | Direction | What it covers |

1 | Purchased goods and services | Upstream | Raw materials, office supplies, professional services |

| 2 | Capital goods | Upstream | Machinery, buildings, IT equipment |

| 3 | Fuel- and energy-related activities | Upstream | Extraction and transmission losses not already in scope 1 or 2 |

| 4 | Upstream transportation and distribution | Upstream | Inbound logistics, third-party warehousing |

| 5 | Waste generated in operations | Upstream | Landfill, recycling, wastewater treatment |

| 6 | Business travel | Upstream | Flights, hotels, rail |

| 7 | Employee commuting | Upstream | Staff travel to and from work |

| 8 | Upstream leased assets | Upstream | Emissions from assets you lease from others |

| 9 | Downstream transportation and distribution | Downstream | Outbound logistics to end customer |

| 10 | Processing of sold products | Downstream | Emissions when another company processes your intermediate product |

| 11 | Use of sold products | Downstream | Energy consumed when customers use your product |

| 12 | End-of-life treatment of sold products | Downstream | Disposal, recycling, incineration |

| 13 | Downstream leased assets | Downstream | Emissions from assets you lease to others |

| 14 | Franchises | Downstream | Emissions from franchise operations |

| 15 | Investments | Downstream | Emissions from equity or debt investments |

Not every category is material for every company. A software business will have negligible Category 10 emissions, for example, while a car manufacturer will have enormous Category 11 emissions. Your first step is identifying which categories represent a significant share of your business’ total footprint. For a full breakdown of each category and what it means for your business, read our in-depth explainer guide to all 15 scope 3 categories.

The graphic below displays a business’s upstream and downstream activities, as well as the 15 categories of scope 3 emissions defined by the Greenhouse Gas Protocol:

See how companies like yours map their full value chain in weeks

Learn more about the categories of scope 3 emissions and what they mean for your business’s carbon management strategy.

30 min. No obligation. Free expert call.

Book a demo

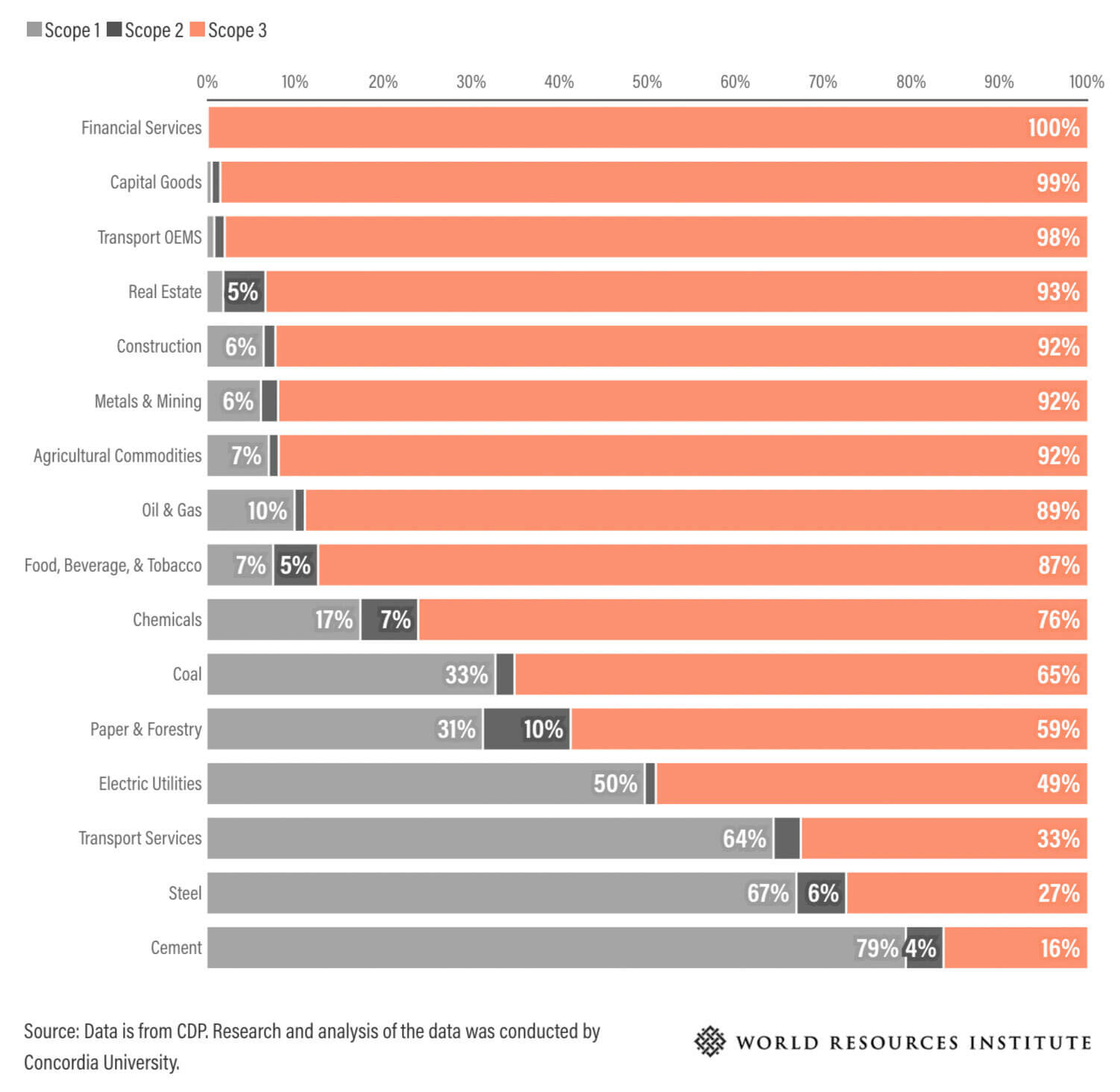

While scope 3 emissions tend to be the largest source of emissions for most companies, there are stark differences across sectors.

On the high end, scope 3 emissions account for 99.98% of emissions in the financial services sector; on the low end, they are responsible for only 16% of emissions in the cement industry.

The graph below from the World Resources Institute breaks down the average emissions of 16 sectors, with data sourced from CDP:

Why are scope 3 emissions important for your business to address?

Across sectors, scope 3 emissions account for approximately 75% of greenhouse gas emissions. In sectors like Capital Goods emissions from Scope 3 Category 11 alone can account for around 90% of the total.

This means that for most companies scope 3 is not a peripheral concern, it is the majority of the climate footprint. Measuring and managing scope 3 is essential to credible emissions reporting, realistic net-zero planning, and regulatory compliance.

The regulatory case

Two major frameworks are driving mandatory scope 3 reporting:

CSRD (Corporate Sustainability Reporting Directive)

The EU’s CSRD requires in-scope companies to report scope 1 and 2 emissions and, where material, scope 3 value chain emissions under the European Sustainability Reporting Standard E1 (ESRS E1). Even though Omnibus I led to less comprehensive scope 3 reporting requirements being signed off by the European Parliament in December 2025, the businesses that remain in scope still need a granular view of their supply chain emissions. And for their suppliers, being able to provide good quality scope 3 data can provide an important competitive advantage.

We’ll cover this in more detail in the ‘Scope 3 reporting requirements’ section.

SBTi (Science Based Targets initiative)

SBTi requires companies seeking SBTi validation to set scope 3 reduction targets when scope 3 represents 40% or more of total emissions. Given that most companies exceed this threshold, scope 3 target-setting is effectively mandatory for any company seeking SBTi validation.

The business case

Compliance is the floor, not the ceiling. Companies that measure scope 3 gain three practical advantages:

- Supply chain risk visibility. Understanding where your emissions concentrate reveals where you may be exposed to carbon pricing, resource scarcity, and supplier disruption, before these risks hit your cost base.

- Cost reduction opportunities. High-emission activities often correlate with high-cost activities: energy-intensive logistics, wasteful procurement, inefficient material use. Scope 3 data frequently surfaces savings opportunities that would otherwise stay hidden.

- Customer and investor credibility. Procurement teams increasingly request scope 3 data from suppliers. Investors and lenders use it to assess transition risk. Credible numbers are a competitive differentiator, not just a reporting exercise.

How to measure scope 3 emissions

Scope 3 measurement is a progression from rough financial estimates to precise primary data. The GHG Protocol defines three main approaches: spend-based (multiplying procurement spend by industry-average emission factors: fast to deploy but less precise), activity-based (using physical quantities such as tonnes purchased or kilometres travelled, for greater accuracy), and supplier-specific (using primary emissions data reported directly by your suppliers. The most accurate but the most demanding to collect). Most companies use all three in combination, shifting more of their inventory toward primary data over successive reporting cycles.

For a full breakdown of each method, when to use it, and how to build a hybrid approach, read our guide, ‘How to calculate scope 3 emissions: from spend data to supplier data.’

How do businesses reduce scope 3 emissions?

Reducing scope 3 emissions is challenging, as these emissions are outside of your company’s direct control.

The first step to reducing scope 3 emissions is to comprehensively and accurately account for them – after all, you can’t manage what you haven’t measured.

Businesses calculate their emissions through a process called carbon accounting. Because scope 3 emissions occur outside your business’s owned operations, it can be challenging to collect the data necessary for value chain carbon calculations, though automated solutions can accelerate the process.

The supplier engagement challenge

Here is the core difficulty of scope 3: most of the data you need lives within other companies.

According to CDP, fewer than half of companies that request environmental data from their suppliers actually receive it. The reasons are predictable: suppliers lack measurement capability, fear exposing competitive information, or simply do not prioritize the request.

Effective supplier engagement follows a clear pattern. For a detailed step-by-step approach, read our guide to supplier engagement for scope 3: how to collect primary data.

- Start with materiality. Identify which suppliers contribute the most to your footprint. Scope 3 Category 1 (purchased goods and services) typically dominates, often 50% or more of total scope 3 for manufacturing and retail companies.

- Make it easy. Provide templates, tools, or platforms that reduce the reporting burden on suppliers.

- Create mutual value. Frame the conversation around shared benefits such as cost savings, risk reduction and preferred supplier status. Don’t just focus on your reporting needs.

- Be patient but persistent. Supplier data quality improves over cycles. Year-one data should be treated as a starting point, but by year three the data should be genuinely useful.

The companies making the most progress on scope 3 treat supplier engagement as a procurement function, not a sustainability side project. See how Normative’s supply chain engagement platform supports this →

What do CSRD and SBTi require for scope 3?

Scope 3 reporting is shifting rapidly from voluntary best practice to regulatory requirement. Here is what the two most significant frameworks require.

What CSRD requires

As of May 2026, the revised version of the European Sustainability Reporting Standards (ESRS) is going through a final round of feedback. Once finalized it will require companies within the scope of the Corporate Sustainability Reporting Directive to:

- Report on material emissions throughout their supply chains

- Double materiality is still mandatory – businesses are required to assess impact and financial materiality, including scope 3

- Adhere to a ‘value chain cap’ which states that companies with less than 1000 employees cannot be required by in-scope businesses to share any information on their carbon emissions beyond what is laid out in the Voluntary SME Standard (VSME).

While scope 3 requirements under CSRD are not as comprehensive as they were pre-Omnibus, and expectations of primary data have been relaxed, there is still a very real competitive element to consider. Voluntary requests for scope 3 data can still be lodged, and suppliers will be very well aware that if they don’t share the carbon emissions data that their bigger customers are requesting, they could put themselves at a competitive disadvantage.

The businesses in-scope of CSRD themselves will need to be able to target the highest-impact areas within their supply chains due to the shift to the risk-based due diligence approach. This means they will still need granular, high quality scope 3 data from their suppliers if they are to meet CSRD requirements.

What SBTi requires

For companies seeking validation under the Science Based Targets initiative:

- Companies where scope 3 represents 40% or more of total emissions must set a scope 3 reduction target

- Near-term targets must cover at least 67% of scope 3 emissions

- The Net-Zero Standard requires a 90% reduction by 2050

For a full breakdown of what each framework requires, read our guide to ‘Scope 3 reporting under CSRD and SBTi: what you actually need.’

See how companies like yours map their full value chain in weeks

Normative’s platform is built specifically for the complexity of value chain emissions measurement and reduction.

Comprehensive emission factor coverage. 349,000+ emission factors (EFs) from 21 scientific databases, providing sector and region-specific EFs to deliver the granularity and reliability businesses need.

All the measurement methods, in one platform. Normative supports spend-based, activity-based, and supplier-specific approaches, as well as product-level emissions, tracking your data quality progression across categories over time.

Carbon Network for supplier data collection. A structured workflow for requesting, collecting, and verifying primary emissions data directly from your suppliers.

EcoVadis integration. Verified supplier intensity data flows directly into your scope 3 calculations without manual data entry.

Proven at scale. Hitachi Rail used Normative to increase its scope 3 coverage from 15% to 90%.

Expert guidance on every account. Every Normative account includes a named, GHG Protocol-certified Climate Strategy Advisor. Normative’s co-founder serves on the GHG Protocol Scope 3 Technical Working Group, the group that writes the standard.

FAQs

Frequently asked questions about scope 3 emissions

Scope 3 emissions are all the indirect greenhouse gas emissions that occur across a company’s value chain, both upstream (supply chain) and downstream (product use and end-of-life), from sources the company does not own or control. Also called value chain emissions, they are defined by the Greenhouse Gas Protocol across 15 categories, and typically account for 70-90% of a company’s total carbon footprint.

Scope 3 emissions account for approximately 70-90% of greenhouse gas emissions across sectors, meaning they are where the majority of climate impact, regulatory obligation, and commercial risk sits. Ignoring scope 3 means reporting an incomplete footprint, setting targets that cannot achieve real-world emissions reductions, and missing the supply chain risk signals that matter most to investors and customers.

Across sectors, scope 3 emissions account for approximately 70-90% of greenhouse gas emissions. The range is wide: in financial services, scope 3 can exceed 99% of total emissions; in cement and heavy industry, it may be as low as 16%. For most mid-market companies in manufacturing, retail, transport, and professional services, scope 3 will represent the significant majority of the total footprint.

Scope 3 emissions are calculated using carbon accounting methods defined in the GHG Protocol Corporate Value Chain Standard. The three main approaches are: spend-based (using procurement spend and average emission factors), activity-based (using physical quantities such as tonnes purchased or kilometres travelled), and supplier-specific (using primary data reported directly by suppliers). Most companies take a hybrid approach, using spend-based for the long tail, activity-based where physical data exists, and supplier-specific for the highest-impact categories.

For a full walkthrough of each method, read our guide to how to calculate scope 3 emissions: from spend data to supplier data.

The data lives outside your organization. You depend on suppliers, logistics providers, and customers for information they may not track themselves, and that they may not be willing to share. The 15 categories add structural complexity. And unlike scope 1 and 2, there is no single data source to draw from. Most companies start with spend-based financial estimates and progressively replace them with more accurate activity-based and supplier-specific data over multiple reporting cycles.

Under the EU’s CSRD, companies meeting certain employee count and revenue thresholds must report scope 3 emissions in line with the ESRS (revised version in review May 2026). SBTi requires scope 3 targets for any company where scope 3 exceeds 40% of total emissions, a threshold most companies exceed. Beyond regulatory obligations, large customers and investors increasingly expect scope 3 disclosure from supply chain partners, even when it is not yet legally mandated in their jurisdiction.

Category 1 (purchased goods and services) dominates for most companies, often 50% or more of total scope 3 emissions for manufacturers and retailers. Other commonly material categories include Category 4 (upstream transportation), Category 6 (business travel), Category 11 (use of sold products, especially relevant for consumer electronics and automotive), and Category 15 (investments, which dominates for financial institutions). Read our full guide to all scope 3 categories explained.

A first spend-based estimate across all relevant categories can be completed in weeks if procurement data is accessible. Activity-based calculations typically take one to two reporting cycles to build properly though, while reaching supplier-specific primary data for your top emitters is a multi-year effort. But each cycle delivers better data, more defensible numbers, and more actionable insights for reduction.

Appendix: scope 3 emissions categories as defined by the Greenhouse Gas Protocol

Refer to the Greenhouse Gas Protocol’s Technical Guidance for Calculating Scope 3 Emissions for a more detailed breakdown of the categories.

Upstream emissions scope 3 categories

| Category | Description |

|---|---|

| Purchased goods and services | Extraction, production, and transportation of goods and services purchased or acquired by the company |

| Capital goods | Extraction, production, and transportation of capital goods purchased or acquired by the company |

| Fuel- and energy-related activities | Extraction, production, and transportation of fuels and energy purchased or acquired by the company which are not already accounted for in scope 1 or scope 2 |

| Upstream transportation and distribution | Transportation and distribution of products purchased by the company, as well as other transportation and distribution services like inbound logistics, outbound logistics, and transpiration between company facilities |

| Waste generated in operations | Disposal and treatment of waste generated in the company’s operations, in facilities not owned or controlled by the company |

| Business travel | Transportation of employees for business-related activities in vehicles not owned or operated by the company |

| Employee commuting | Transportation of employees between their homes and their worksites in vehicles not owned or operated by the company |

| Upstream leased assets | Operation of assets leased by the company and not included in scope 1 and scope 2 |

Downstream emissions scope 3 categories

| Category | Description |

|---|---|

| Downstream transportation and distribution | Transportation and distribution of products sold by the company between the company’s operations and the end consumer |

| Processing of sold products | Processing of intermediate products sold by downstream companies |

| Use of sold products | End use of goods and services sold by the company |

| End-of-life treatment of sold products | Waste disposal and treatment of products sold by the company, at the end of the products’ lives |

| Downstreamleased assets | Operation of assets owned by the company and leased to other entities |

| Franchises | Operation of franchises in the reporting year, not included in scope 1 and scope2 |

| Investments | Operation of investments, including equity and debt investments and project finance |