Carbon is a business variable, not a compliance chore

CFOs need to think about sustainability differently. Here's why.

Nobody put sustainability on my job description. Like most CFOs I’ve spoken to, it arrived somewhere between legal, audit prep and a regulatory deadline, and landed on their desk because it involved numbers and someone had to own it. That’s not a complaint. It’s just how the CFO role works, especially in smaller businesses where your remit ends up being as wide as it is varied.

What I’ve come to believe, though, is that how sustainability arrives matters a lot less than what you decide to do with it once it’s there. And right now, I think a lot of CFOs are making the wrong call.

The compliance-first approach costs more than you think

When sustainability reporting enters the business through a regulatory door, the natural instinct is to treat it accordingly – scope it carefully, assign it to whoever has capacity, get it done. If your investors aren’t pushing hard on it, doing the minimum is a defensible position, and I’ve seen boards with private equity backing explicitly tell management to limit ESG reporting to whatever compliance requires. Nothing more.

The problem with that approach isn’t that it’s wrong in principle. It’s that it misreads what the data is actually worth.

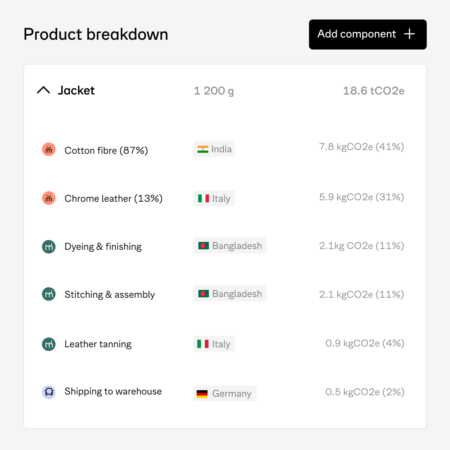

A rigorous, traceable account of your full emissions footprint is not just a regulatory artefact. It’s a signal that travels into procurement decisions, investor due diligence, supply chain risk assessments, and increasingly, credit conditions. When 78% of senior executives agree that ESG performance contributes to financial value, and consumers are willing to pay an average premium of 27% for brands delivering on sustainability promises, the question stops being ‘do we have to report?’ and becomes ‘what are we leaving on the table by not taking this seriously?

That reframe is the CFO’s job. Nobody else in the room is going to make it.

Use the toolkit you already have

Here’s what I actually find clarifying about this: the skills you need to make a compelling case for sustainability investment are exactly the skills CFOs already use every day. Data analysis. Financial modelling. Cross functional persuasion. Storytelling to a board.

If you face resistance – from a CPO who thinks sustainability belongs to someone else, or a CEO who wants to defer until regulations force the issue – the answer isn’t to argue on environmental grounds.

- Build the ROI model.

- Show what better carbon data means for procurement eligibility.

- Quantify the audit risk of inaccurate scope 3 reporting.

- Map the emissions hotspots in your supply chain and connect them to cost reduction.

Frame it the way you’d frame any capital allocation decision: what is the return, and what is the cost of inaction?

This is where CFOs have a genuine edge. We’re trained to pull disparate data into a coherent narrative and manage C-suite relationships across competing priorities. That capability is exactly what sustainability advocacy requires inside most organizations. The companies I’ve seen move fastest on this aren’t the ones with the largest sustainability teams. They’re the ones where finance decided to treat carbon as a business variable rather than a reporting obligation.

Why complexity in the market actually strengthens the case for rigor

I’ll be honest: the climate tech landscape is more complex than most people outside it appreciate. Regulations shift. Geopolitical pressures create unexpected deregulatory moves in some markets even as others tighten. Macroeconomic conditions influence what boards are willing to prioritize in any given quarter.

That complexity is real, and any CFO who tells you the regulatory trajectory is perfectly predictable is oversimplifying. But I think uncertainty in the external environment is actually the argument for having data you can rely on internally. If the rules are shifting, you want a carbon footprint calculation that is traceable, consistent year over year and defensible under audit. Spreadsheet-based approaches don’t give you that. Estimates built on spend proxies don’t give you that.

The CFOs who navigate this period well will be the ones who built the data infrastructure while the rules were still forming, not the ones scrambling to reconstruct their numbers when a new regulation or investor questionnaire demands something specific.

A personal note on why I’m here

I spent a decade in fintech before joining Normative. I made the move because I wanted to work somewhere where the end goal of the business actually matters – not just to the P&L, but in the world. That’s a personal thing and I don’t think every CFO needs to share it to do this work well.

What I do think is that the CFOs who approach carbon accounting with genuine curiosity, who want to understand what the data is telling them about their business, not just how to satisfy an auditor, are going to be better positioned than those who don’t. Not because it’s the right thing to do. Because that’s where the value is.

Two questions I’d put to any CFO reading this

- If your carbon data turned out to contain material errors tomorrow, particularly in your scope 3, how confident are you that you’d know, and how quickly could you actually correct it?

- When you think about the ROI of sustainability reporting in your organization, are you genuinely modelling it, or are you assuming it’s a cost center because nobody has built the case yet?

Those two questions have shaped how I think about this. I suspect they’ll be useful for others too.

Want to untap the ROI of sustainability reporting?

Read our C-suite guide to carbon accounting ROI to see the wider business value you could deliver.