What is a CSRD double materiality assessment?

A DMA reveals your business's key impacts, risks, and opportunities – driving smarter strategies & CSRD compliance

A double materiality assessment (DMA) is mandatory per the Corporate Sustainability Reporting Directive (CSRD). However, double materiality has value for your business far beyond compliance.

A strong double materiality assessment reveals your business’s risks and opportunities across areas like climate change, biodiversity, and corporate governance While a weak DMA will not only put your compliance at risk – it will also leave you unaware of financial and environmental risks throughout your operations.

Here’s what double materiality means, why it’s important for CSRD and beyond, and how your business can conduct a double materiality assessment.

Defining double materiality

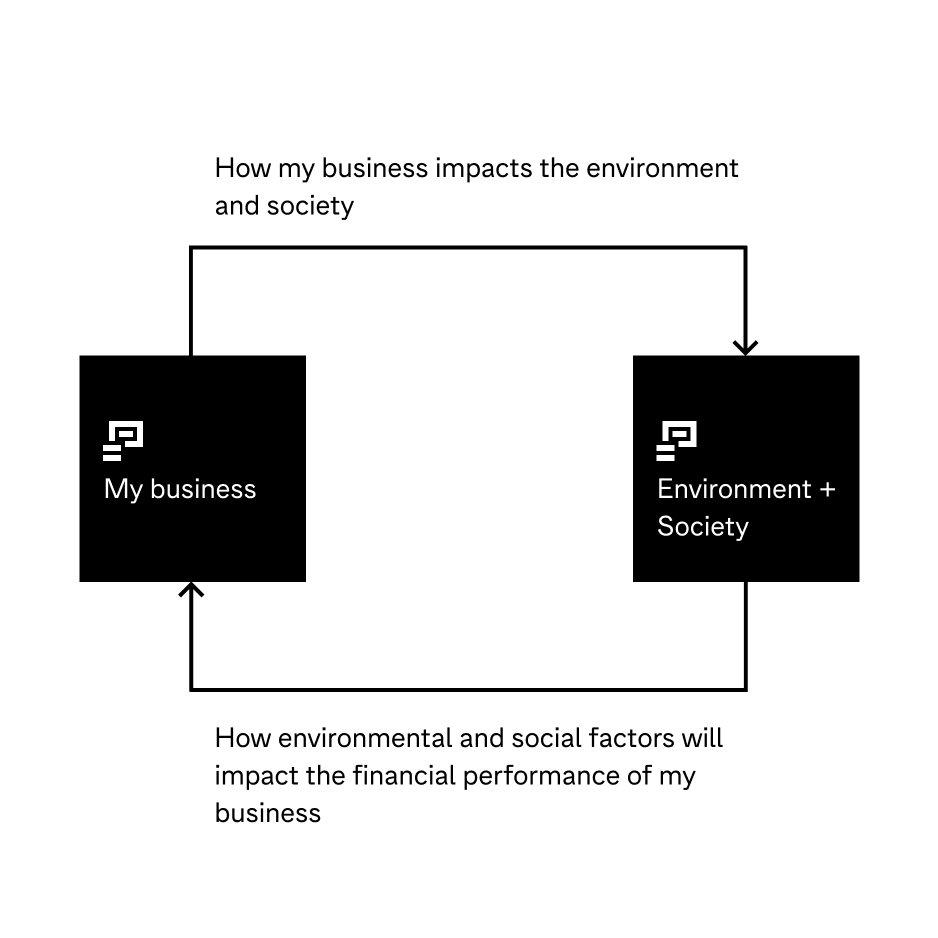

Double materiality is holistic approach to assessing impact. It acknowledges business risks and opportunities from both financial and non-financial perspectives.

A double materiality assessment assesses a company’s impacts on the environment and society (impact materiality) alongside how sustainability issues affect the company’s financial performance (financial materiality), providing a comprehensive view of a business’s role in and relationship with the broader world.

The table below breaks down the two kinds of materiality, with examples:

| Two kinds of materiality | Examples |

|---|---|

| Impact materiality: Your business’ positive and negative impacts on the environment and society. Also known as “inside-out” impacts. | Carbon emissions: A business’ greenhouse gas emissions contribute to climate change, impacting global temperatures and weather patterns. Waste management: Improper waste disposal by a business can lead to pollution, affecting local ecosystems and community health. Labor practices: A business’ labor practices, such as ensuring fair wages and safe working conditions, can significantly affect the well-being and economic stability of its employees and their communities. |

| Financial materiality: The potential risks and opportunities from the environment and society on your business’ financial performance. Also known as “outside-in” impacts. | Climate change regulations: New regulations aimed at reducing carbon emissions could increase operational costs for businesses reliant on fossil fuels, impacting their financial performance. Consumer preferences: A growing consumer preference for sustainable products can drive sales for businesses that invest in eco-friendly products, boosting their financial outlook. Supply chain disruptions: Environmental events, such as floods or hurricanes, can disrupt supply chains, affecting production and leading to financial losses. |

Financial and impact materiality are interconnected: a company’s impact on the environment or society can often lead to financial risks or opportunities, and vice versa.

For example, consider a hypothetical company that switches to sustainable packaging for its products.

This decision reduces plastic waste (impact materiality) but initially increases costs.

However, this decision soon leads to increased earnings (financial materiality) because environmentally-conscious consumers prefer the product; the improved brand image attracts new customers and investors; and the company becomes less vulnerable to supply chain disruptions in petroleum-based packaging.

What began as an environmental initiative ultimately increased revenue and reduced risks. This interconnectedness between financial and impact materiality is at the core of double materiality.

Single vs. double materiality: what’s the difference?

Traditional “single materiality” focuses only on how sustainability issues affect a company’s financial performance and value. For example, a single materiality assessment would consider how climate change might disrupt your supply chain, but not how your operations contribute to climate change.

Double materiality takes a broader view by considering both financial impacts and your company’s effects on the environment and society. This comprehensive approach, required by CSRD, provides a fuller picture of your business’s sustainability risks and opportunities, enabling more effective strategy and risk management.

Double materiality in CSRD reporting

The CSRD explicitly requires companies to apply the concept of double materiality in their sustainability reporting.

Double materiality is part of ESRS 1 “General requirements,” which is mandatory for all reporting companies.

Key CSRD requirements related to double materiality include:

- Conducting a double materiality assessment to identify relevant sustainability topics

- Disclosing the process used to determine material topics

- Reporting on both the actual and potential impacts of the company’s operations

- Explaining how sustainability issues affect the company’s business model and strategy

For a straightforward and comprehensive breakdown of double materiality’s relevance to CSRD reporting, download Normative’s handbook to decoding the CSRD.

Decoding CSRD

How to comply with the Corporate Sustainability Reporting Directive (CSRD) and gain real business value in the process.

Download

How to conduct a double materiality assessment

The process for completing a double materiality assessment is similar to the overall process of completing your CSRD disclosure. You plan, assign responsibility, collect information, process information, align with leadership, and submit.

The core of that process – effectively analyzing the factors that may be material for your business, and determining their significance – is the most important part to get right. Below is a simplified four-step plan to help you do so!

Determining materiality: a four-step plan

- Analyze your business

Look closely at your business operations, from sourcing materials to delivering products or services. Identify who your stakeholders are (like employees, customers, suppliers, and local communities) and how your business might affect them and the environment. Don’t forget to consider the suppliers and service providers that make up your supply chain.

- Find actual and potential impacts, risks, & opportunities

Talk to the stakeholders you’ve identified to discover how your business actually affects or could affect people and the environment, both positively and negatively. For example, consider things like your carbon emissions, waste production, employment practices, and community contributions.

You should also consider the financial risks and opportunities related to these impacts. For instance, a company might identify that its reliance on fossil fuels poses a financial risk due to potential carbon taxes or changing regulations. Conversely, investing in renewable energy could present an opportunity to reduce long-term energy costs and appeal to environmentally conscious consumers.

- Evaluate double materiality

Determine the significance of each impact, risk, and opportunity. Consider how grave the impact is (scale), how widespread the impact is (scope), and the extent to which the impact can be reversed (irremediability). Use precise numbers (e.g. carbon emissions broken down by scope & category) and descriptions (e.g. employee satisfaction levels) to assess materiality. This should be done scientifically and objectively. It’s also advisable to undergo external auditing once the DMA is finalized.

Materiality is determined by either, or both:

Impact materiality: it affects communities and the environment, in a positive or negative way.

Financial materiality: it affects your business’ financial success, in that it brings either opportunities or risks

- Choose key issues to address

Based on your assessment, decide which issues are the most crucial for your business to focus on. These should be the topics that have the biggest positive or negative impacts, the highest amount of risk, or the greatest opportunities for your business success, your stakeholders, and the external environment. These are the issues you’ll need to report on in CSRD and work to improve.

This plan was adapted from Normative’s handbook Decoding CSRD

By following this process, you’re not just ticking a compliance box. You’re gaining invaluable insights into your business’s relationship with the environment and society.

This deeper understanding allows you to identify areas where you can make the most significant positive impact and where you face the greatest risks, enabling you to focus your sustainability strategy more effectively.

How often to conduct a DMA

Double materiality is an ongoing process, not a one-and-done project. Your double materiality assessment (DMA) should evolve with your business and the world around it.

Update your DMA when there are material changes in your organizational or operational structure, or when external factors could create new impacts, risks, and opportunities (IROs) or modify existing ones.

For CSRD reporting, your DMA should be revisited annually. This regular review ensures your sustainability reporting remains current, accurate, and aligned with both your business realities and CSRD requirements.

Using double materiality for strategic advantage

While your initial motivation for conducting a DMA may be for reporting reasons, the benefits you get from it needn’t stop at compliance!

A double materiality assessment gives you a deeper understanding of your business. You can use it to identify the areas where you have the potential to make the biggest impact, then focus your strategy on these areas.

This can unlock benefits including improved risk management, enhanced stakeholder engagement, and driving innovation.

The business benefits of a thorough DMA:

- Improved risk management:

By considering both impact and financial materiality, you can identify and mitigate a broader range of risks. - Enhanced stakeholder engagement:

The process of assessing double materiality involves continuous dialogue with your stakeholders, and fostering better relationships. Sharing the results of your assessment and your plans to improve on key challenges builds trust. - Driving innovation:

Understanding sustainability impacts can lead to product and process innovations that reduce negative impacts and create new business opportunities.

Executive summary

Double materiality is an approach that acknowledges business risks and opportunities from both financial and non-financial perspectives.

It’s an essential element of sustainability reporting and a requirement for complying with CSRD. However, it isn’t just a compliance box to tick: it’s a way to understand your business’s relationship with the world around it.

A thorough double materiality assessment helps you identify key sustainability issues, engage meaningfully with stakeholders, manage risks more effectively, and drive innovation. It’s an ongoing process that, when done right, can transform your sustainability reporting from a compliance exercise into a strategic advantage.

“Normative has been a great support to Aasted’s CSRD preparation”

Jesper Jerlang, Sustainability Manager at Aasted, uses Normative for CSRD reporting.

Learn how you, too, can keep your business compliant – and drive emissions reductions – by booking a demo of Normative.

Book a demo

FAQs

Frequently asked questions about double materiality & CSRD

Double materiality is a reporting approach that assesses two key aspects: how sustainability issues affect a company’s financial performance (financial materiality), and how the company impacts the environment and society (impact materiality). Required by the EU’s Corporate Sustainability Reporting Directive (CSRD), double materiality helps businesses understand their full sustainability risks, impacts, and opportunities.

Single materiality only considers how sustainability issues affect a company’s financial performance and value. Double materiality takes a broader view: it considers both financial impacts AND how the company affects the environment and society. Required by the EU’s Corporate Sustainability Reporting Directive (CSRD), double materiality provides a more comprehensive understanding of a company’s sustainability risks, impacts, and opportunities than single materiality.

You should update your DMA when there are any material changes in your organizational and operational structure, or in the external factors that could generate new or modify existing impacts, risks, and opportunities (IROs). For CSRD, the DMA is done once and then revisited annually.

Failing to properly apply double materiality could result in incomplete or inaccurate reporting, potentially leading to regulatory non-compliance, reputation damage, and missed opportunities for risk management and value creation.

Key factors include thorough stakeholder engagement, using recognized methodologies and data sources, ensuring transparency in your process, documenting your value chain, and considering external verification of your assessment. It’s also beneficial to work with an experienced partner with specific CSRD expertise.